Tiny Sushi Spot in Boca - Not Shuko Good, But Pretty Darn Good

9-16-21

Opening Comments

Picture of the Day-Rates Chart

Quick Bites

Markets, Dunkin Donuts/Global Labor, Clean Energy

Steel/Uranium Prices, CPI, Apple, China Gaming Stocks

Democratic Tax Proposal/NYC Effective Wealthy Tax/Estate Taxes

Facebook-Faceplant, New NYC Restaurants, Speed Toading

Virus/Vaccine

Data

Vaccine Ages 5-11

Singapore/Israel Woes Despite Vaccinations

Alabama Horror Story

Real Estate

My Views (more examples)

NYC Rents on the Rise/Story from my NYC Rent Experience

JPM Real Estate Analysis-There is No Place Like Home

UK Home Prices

Opening Comments

I will be 52 years old in November. I have battled back issues (L4/L5-L5-S1) for almost 15 years. I throw out my back from time to time and it is not in a good way now. I feel like an invalid. It is hard to walk and I am in agony. I wont take heavy pills and my normal back guy is on holiday. I think I am breaking down and going to try yoga, something I have never done. Getting old is for the birds. I was unable to finish my piece on Wednesday because I was in too much pain. Here is the late Jewish Holiday send to check out over the weekend.

Today’s piece is a little longer as there was just too many things I wanted to share. Check the list to see which Quick Bites interest you. There are some good ones today. If you are pressed for time, I ask that you read the Facebook point in Quick Bites. I don’t care what side of the isle you sit, this should concern you.

The readership continues to expand and want to remind everyone to send me thoughts, feedback story ideas. Some of my best Quick Bites are from readers. I can only find so much on my own. If it is interesting to you, probably interesting to all.

Picture of the Day

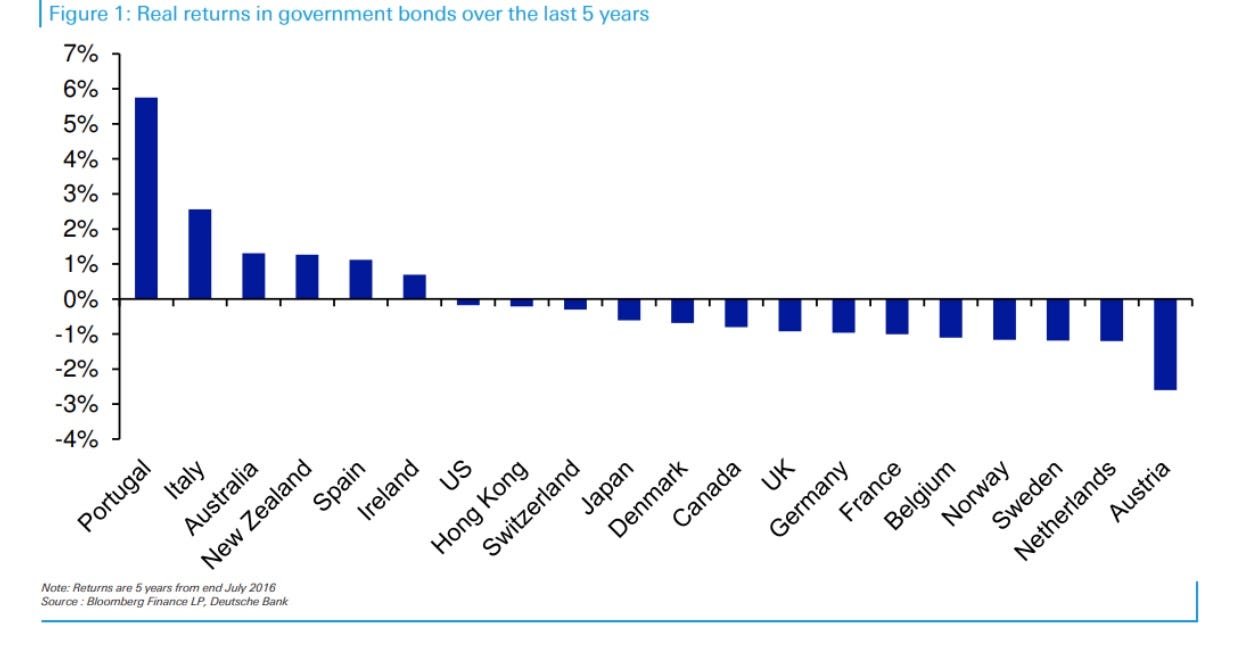

From time to time, I insert a section from DB’s Jim Reid who writes a daily thought piece on the market. I found this one interesting about real rates. What are the long-term ramifications for those who are reliant on fixed income (insurance, pension, endowments, retirees…).

After four decades of stunning real (and nominal) returns in fixed incomes, the gravitational pull to zero is catching up with us. Today’s piece shows that real returns in government bonds are now negative across a number of countries in the five years to the end of July (the last point for all inflation data to be available). Even the US is slightly negative now because although 10yr yields were still c.1.5% in July 2016, annual inflation has averaged above this over the period.

These negative returns shouldn’t be a surprise when you have no or negligible coupons and any kind of inflation, but it’s a reminder of the immense financial repression at hand, and it’s probably the first time in over 40 years that the rolling 5-year real return for so many government bonds is now negative. Obviously the EU periphery and higher yielding bond markets have still seen positive real returns over the last 5 years given their July 2016 starting point but at current yields they will now struggle to replicate this going forward.

So although yields continue to defy the consensus and remain around rock bottom levels around the world, those that have remained bullish aren’t really benefitting in return terms from correctly identifying that yields wouldn’t rise. It still seems an asymmetric risk reward asset class from here unless you believe CBDC will revolutionise interest rate setting in the years ahead and allow rates to go deeply negative and drag bond yields even further down as a result thus allowing capital gains to offset large negative carry.

Tiny Sushi Spot in Boca - Not Shuko Good, But Pretty Darn Good

I have been crystal clear that the food choices in Boca and generally in Florida are a far cry from the greatness of NYC’s choices. I am a lover of high quality sushi and have been shocked at the paucity of choices down here. We are on the ocean with fresh tuna, yellowtail, snapper, wahoo, grouper, amberjack, shrimp….yet the sushi is horrible. My favorite sushi in NYC was always Shuko on 12th Street. It is a small Omakase only restaurant which serves up an amazing experience for those lucky enough to try it. If I were to be on my death bed and could have one last bite of food, I think it would be the fatty tuna from Shuko.

I have struggled mightily down in Boca and actually started catching my own sushi. I have a boat and fish a lot and catch fresh tuna, dolphin, wahoo, snapper, grouper… No, it aint Shuko, but beats the crap down here until today.

50 lb Wahoo-Bimini

15 lb Black Fin Tuna

I seared the tuna (1 minute on each side) and it looks like this when done with crushed peppercorn on the sides.

Sunset Sushi

2433 North Federal Highway

Boca Raton, FL 33431

(561) 405-6049

I was told about Chef Boudadana’s Sunset Sushi, and just tried it for the first time. The chef is American and trained under sushi masters. He lived in Japan and NYC. He was stuck on his boat in NY for 5 months due to the pandemic and watched the sunsets while fishing, hence the name, Sunset Sushi.

It is rare that I am impressed with restaurants in Florida, but wow, Sunset Sushi it is quite good. I ordered for pick up as the restaurant seats only 8 people at the counter and is impossible to get in. I ordered the $80 roll special and the $60 sushi special. I do not believe you can order individual pieces or rolls. This is a lot of high quality sushi for $140. I thoroughly enjoyed the fatty tuna, salmon, yellowtail and snapper. The rolls were solid. However, I did not love the blue crab roll topped with tuna. But apart from that, I was pleasantly surprised to be this impressed with the food, timely service and presentation, as you can see below. They give you a bunch of different sauces, as you can see in the package. I highly recommend ordering from Sunset Sushi, but given the small kitchen, there are limited windows. Order early in the day on line and pick it up at your desired time. FINALLY, a sushi restaurant in Boca which is pretty darn good. NOT Shuko good, but darn good. These were the two boxes of sushi we ordered. I thought he packaging was very well done as well.

This is another review of the restaurant in the Boca Tribune and gives the history of the chef for those interested. The video of Chef Boudadana being interviewed was 5 minutes full of information and worth a look to all those in the vicinity. I read a couple dozen reviews of the restaurant from people who ate inside and it found the feedback to be universally positive. The restaurant is in Boca on Federal Highway, also called US 1, just north of Mizner Boulevard on the West hand side of the street. I believe if you go to the restaurant it is $125/person as the baseline price.

Quick Bites

Shorter markets section today to focus on breadth issues. This week was choppy with the S&P up less than 1% this week, but down 1% on the month. I really enjoyed this CNBC piece on market breadth and a bunch of names down 20% or more from 52 week highs. 15% of S&P 500, 30% of S&P Midcap and 48% of S&P Small Cap are below 52-week highs. The article goes into great detail about specific stocks down decently from recent highs and is meant to show despite the fact that indices are near records, not all stocks are participating.

Industrials/Materials

(% off 52-week highs)

American Airlines 26%

FedEx 20%

Dupont 20%

PPG 18%

Caterpillar 17%

Stanley Black & Decker 17%

Lockheed Martin 14%

3M 12%

Retailers

(% off 52-week highs)

Nordstrom 41%

Gap 36%

Abercrombie 24%

Kohl’s 19%

Ross Stores 16%

The China slowdown, particularly the decline in retail sales due to Covid issues, is dramatically affecting luxury retailers, many of which are based in Europe.

Luxury Retailers

(% off 52-week highs)

Kering 21%

Tapestry 20%

Richemont 17%

Movado 15%

LVMH 14%

Supply chain and labor problems are affecting the ability of some homebuilders to fully deliver on orders.

Home builders

(% off 52-week highs)

Pulte 26%

KB Home 21%

DR Horton 17%

Lennar 11%

I have written extensively about unintended consequences of free money policies. Small and large businesses alike are struggling on the labor front. Alex Apodaca, chief operating officer at JB Partners, an Arizona-based Dunkin Donuts franchisee that manages seven Dunkin' stores in the area, told the outlet: "We just can't get people to work." The west-side Dunkin' on Colorado Avenue has been operating for 55 years. The store would usually have 15 employees on its rotation, But that fell to three just before the store closed, Apodaca said. "We're in a major labor crisis and that is the 100% reason why we're closed," he added. "No other reason." A new kind of Dunkin’ has just opened in Boston. The Canton-based chain is unveiling its first-ever “digital-only” restaurant. It’s located at 22 Beacon Street, next to Boston Common. The location only takes digital orders placed in advance via the Dunkin’ mobile app or at an in-store kiosk, and makes them available for contactless pickup in a designated area. I love this idea. No one wants to work? Get rid of the need for employees and do tasks with less human interaction. Over the next 10 years, how many jobs will be gone due to technology? I spoke with someone in the dental products manufacturing business who has a plan in Ohio. I said, “It must be expensive to pay for US labor.” He let me know there are 3 employees in the plant and everything is done with machines making the need for human interaction far more limited. One of the largest jobs in terms of number employed in the US is driver (truck, taxi, Uber, Lyft, Amazon, Mail, School Bus, City Bus, Fed Ex, UPS…). At what point do we actually see self driving cars become more prevalent? Is it 10 years? 15? 20?

A good Bloomberg article on the difficulty companies face in finding talent. Based on the data, it is more of a global problem. Businesses around the world want to hire but face a similar dilemma: attracting workers. A survey of nearly 45,000 employers across 43 countries showed 69% of employers reported difficulty filling roles, a 15-year high, according to employment-services provider ManpowerGroup Inc. At the same time, 15 countries -- focused in Europe and North America -- reported their highest hiring intentions since the survey began in 1962. “Continued talent shortages mean many businesses are prioritizing retaining and training workers with the skills they need to succeed as the economic recovery continues,” Jonas Prising, chief executive officer of ManpowerGroup, said in a statement.

I want my new readers to understand that I am all for clean energy and lowering emissions. I have owned a Telsa for three years and will again buy another EV. I would like to see a global push for cleaner energy (solar, wind, wave, bio-fuels…). However, I believe it is very unrealistic to think we can rely solely on clean sources any time soon, despite Green New Deal proposals, not to mention the cost. I am not convinced the trillions of dollars projected to get to net zero greenhouse gas emissions in the next 15 years is realistic. I found this article about an interruption in the wind in the North Sea interesting. Again, I would love to see more clean energy, but I am not convinced fossil fuels will be unnecessary in the near future. Natural gas and electricity markets were already surging in Europe when a fresh catalyst emerged: The wind in the stormy North Sea stopped blowing. The sudden slowdown in wind-driven electricity production off the coast of the U.K. in recent weeks whipsawed through regional energy markets. Gas and coal-fired electricity plants were called in to make up the shortfall from wind. Natural-gas prices, already boosted by the pandemic recovery and a lack of fuel in storage caverns and tanks, hit all-time highs. Thermal coal, long shunned for its carbon emissions, has emerged from a long price slump as utilities are forced to turn on backup power sources. The episode underscored the precarious state the region’s energy markets face heading into the long European winter. The electricity price shock was most acute in the U.K., which has leaned on wind farms to eradicate net carbon emissions by 2050. Prices for carbon credits, which electricity producers need to burn fossil fuels, are at records, too.

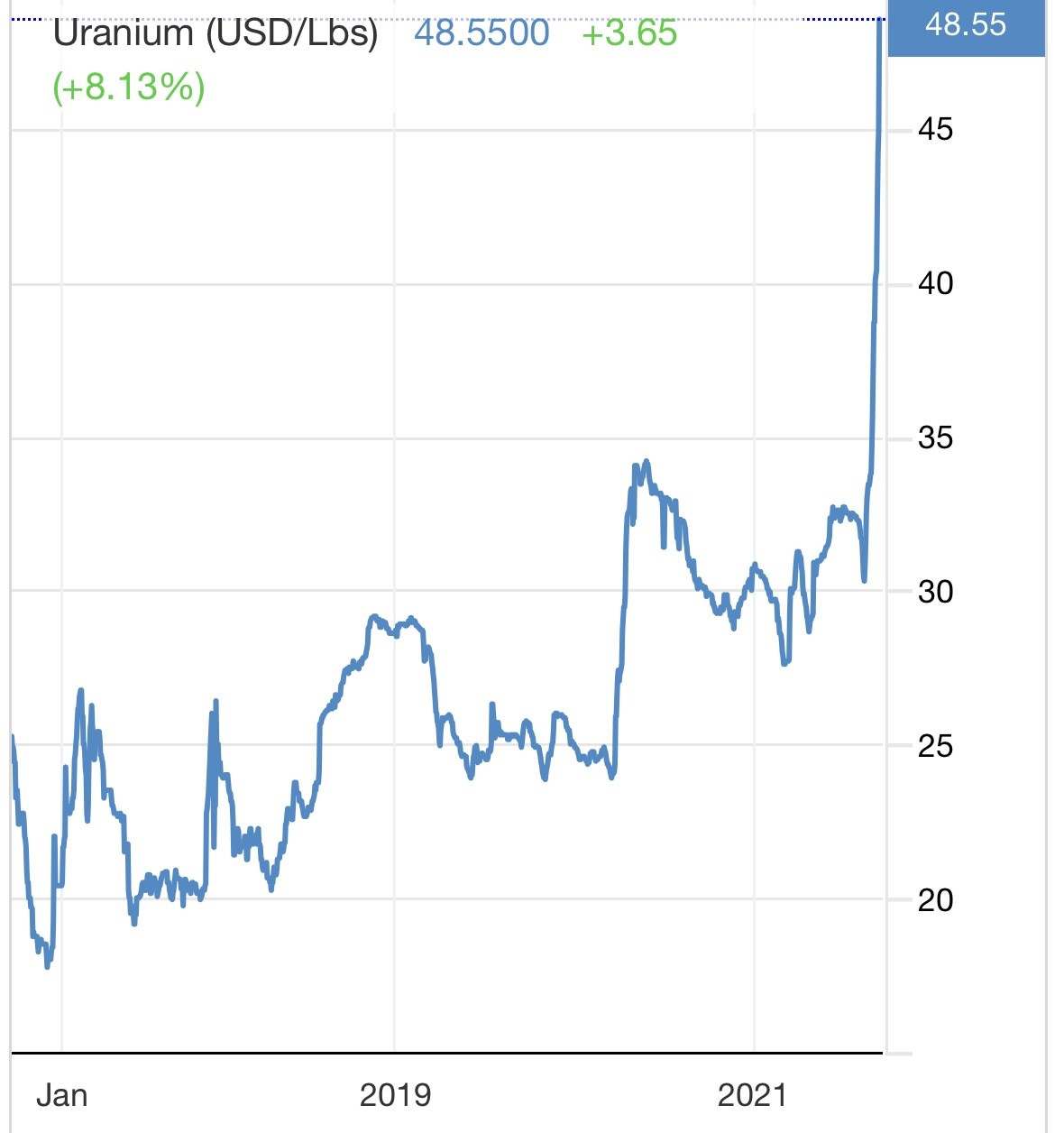

Manufacturers are facing the highest steel and aluminum prices in years, another hurdle for U.S. companies already struggling to make enough cars, cans and other products. Rapidly increasing metal costs are pushing manufacturers to take what steel they can get and hire more people to seek out available supplies, company executives said. The rising costs are flowing through to some producers of consumer goods: Cambell Soup is paying more to get the cans it fills with tomato soup; Peloton is seeing prices rise for parts that go into its stationary bikes; and Steelcase Inc. is paying more to make metal desks and filing cabinets. Car makers like Ford and GM are also dealing with rising metal prices. “It’s crazy for steel,” said Brian Nelson, president of HCC Inc., which sells large metal accessories to tractor manufacturers. “I can’t even get material at times.” Uranium stocks are on fire too. The price of uranium was hovering between $20- $30./lb for 5 years. It is at $47/pound today. In 2007, uranium was $130/l for perspective. Stocks related to uranium are up a lot because of the underlying price given a new trust is buying up to $1bn and due to Reddit.

Prices for an array of consumer goods rose less than expected in August in a sign that inflation may be starting to cool, the Labor Department reported Tuesday. The consumer price index, which measures a basket of common products as well as various energy goods, increased 5.3% from a year earlier and 0.3% from July. A month ago, prices rose 0.5% from June. Economists surveyed by Dow Jones had been expecting a 5.4% annual rise and 0.4% on the month. Stripping out volatile food and energy prices, the CPI rose just 0.1% for the month vs. the 0.3% estimate, and 4% on the year against the expectation of 4.2%. The 5.3% annual increase still keeps inflation at its hottest level in about 13 years, though the August numbers indicate the pace may be abating. Again, last year was horrible, so it is no surprise it is meaningfully higher. When will all the logistics issues return to normal? What about wages and labor? I just fear the pandemic related issues are here to stay for a while. Look at my portion in Virus/Vaccine section on Singapore and Israel. They are highly vaccinated and remain under pressure.

I have an iPhone and iPad. When they first came out, I was AMAZED. I no longer love the products. I have so many issues with my phones. I am over the iPhone, but my family and friends have them and I use Facetime or I would dump them. I am not a phone expert, but listened to analysts comment that approximately 50% of Apple’s sales come from phones and they questioned if the upgrades were big enough to drive similar sales over the next 12 months relative to the last twelve months. Apple kicked off its fall product event on Tuesday by diving right into lots of product announcements.

Here’s what Apple announced:

- The new iPad and iPad mini

- The Apple Watch Series 7

- The iPhone 13 and iPhone 13 mini

- The iPhone 13 and iPhone 13 Pro MaxThe new iPads will go on sale after the event on Tuesday and ship next week. The new iPhones go on sale on Friday, Sept. 17 and ship on Friday, Sept. 24. The Apple Watch Series 7 will ship later this fall. OF note: it didn’t announce new AirPods.

Macau’s top gaming stocks lost a record $18.4 billion in combined market value on Wednesday after officials said they would change casino regulations to tighten restrictions on operators, including appointing government representatives to “supervise” companies in the world’s biggest gaming hub. The Bloomberg Intelligence index of the six big casino operators fell a record 23%. American operators saw the worst selloffs, with Sands China sinking as much as 33%, while Wynn Macau. plunged 34%, both the steepest declines ever. Galaxy Entertainment slumped 20%, its sharpest drop in a decade. Wynn Resorts Ltd., Las Vegas Sands Corp. and MGM Resorts International sank for a second day in U.S. trading. Investing in China is hard. I do not like “stroke of the pen” risk and largely stay away from investments in China.

WSJ article on the Democratic tax proposal. I tried to highlight portions my readers would want to know, but please read the article for yourselves. This is changing daily and lots of articles suggesting SALT laws could be repealed. The basic capital-gains rate would rise to 25% from 20%. When combined with an existing 3.8% investment-income tax and the surtax, the new top rate on capital gains could be as high as 31.8%. The capital-gains tax increase would be effective as of today, with special transition rules for deals with binding contracts that haven’t been completed yet, according to a summary released by the committee. Businesses would face a series of tax increases. The top tax rate would rise to 26.5% from 21%. That is below the 28% that the Biden administration proposed but above the 25% that some Senate Democrats are seeking. Smaller companies would get tax brackets with lower rates. Companies would also face new limits on interest deductions and higher taxes on their foreign income. In several areas, the committee proposed tax increases that weren’t as far-reaching as those the Biden administration has sought. It didn’t include a provision opposed by banks that would have required annual reporting on account flows to the Internal Revenue Service. The House plan doesn’t change the income-tax rules that allow unrealized capital gains to go untaxed at death. Rural Democrats had opposed that administration capital-gains plan, and its chances of becoming law are looking slimmer.

This is a related CNBC story about the tax rates and discusses high tax states (NY and CA) and what the top end effective rate will be under the new Democratic proposal. CNBC is suggesting NYC folks at the high end would be 61.2% and CA would be 59%. I will say this again. I do not believe these tax rates should pass or will pass. I do not believe you can tax yourself to property. Top earners in New York City could face a combined city, state and federal income tax rate of 61.2%, according to plans being proposed by Democrats in the House of Representatives. The plans being proposed include a 3% surtax on taxpayers earning more than $5 million a year. The plans also call for raising the top marginal income tax rate to 39.6% from the current 37%. The plans preserve the 3.8% net investment income tax, and extend it to certain pass-through companies. The result is a top marginal federal income tax rate of 46.4%. The marginal rate is the rate for every dollar above the tax bracket income threshold. In New York City, the combined top marginal state and city tax rate is 14.8%. So New York City taxpayers who earn more than $5 million a year would face a combined city, state and federal marginal rate of 61.2% under the House plan.

Good article in Bloomberg about estate taxes. The latest plan released by House Democrats scales back many of President Biden’s proposals to hike taxes on corporations and rich investors, as moderates and progressives tussle over how far to go to address inequality. But they included an element the White House left out. The package by the Ways and Means Committee calls for a revamp of the U.S. estate-and-gift tax, a levy on the country’s largest fortunes which has been greatly weakened over decades. If House Democrats have their way, rich Americans will soon be scrambling for new and probably more expensive ways to pass wealth onto heirs. The 881-page legislative proposal cracks down on a number of strategies that have made the tax easy to avoid if you hire the right advisers. That could upend how the top 0.1% manages their fortunes and whether they can move millions, sometimes billions, of dollars’ worth of assets outside their estates tax-free. “That’s a huge sea change,” said Brad Dillon, a senior wealth strategist at UBS Group AG in New York. The move eliminates a majority of transactions estate planners would typically advise clients to do, he said. Starting next year, Democrats would make more millionaires subject to the tax, by cutting in half the lifetime exemption — now $23.4 million for a married couple — which is the amount that can be passed on without triggering the 40% estate or gift levy.

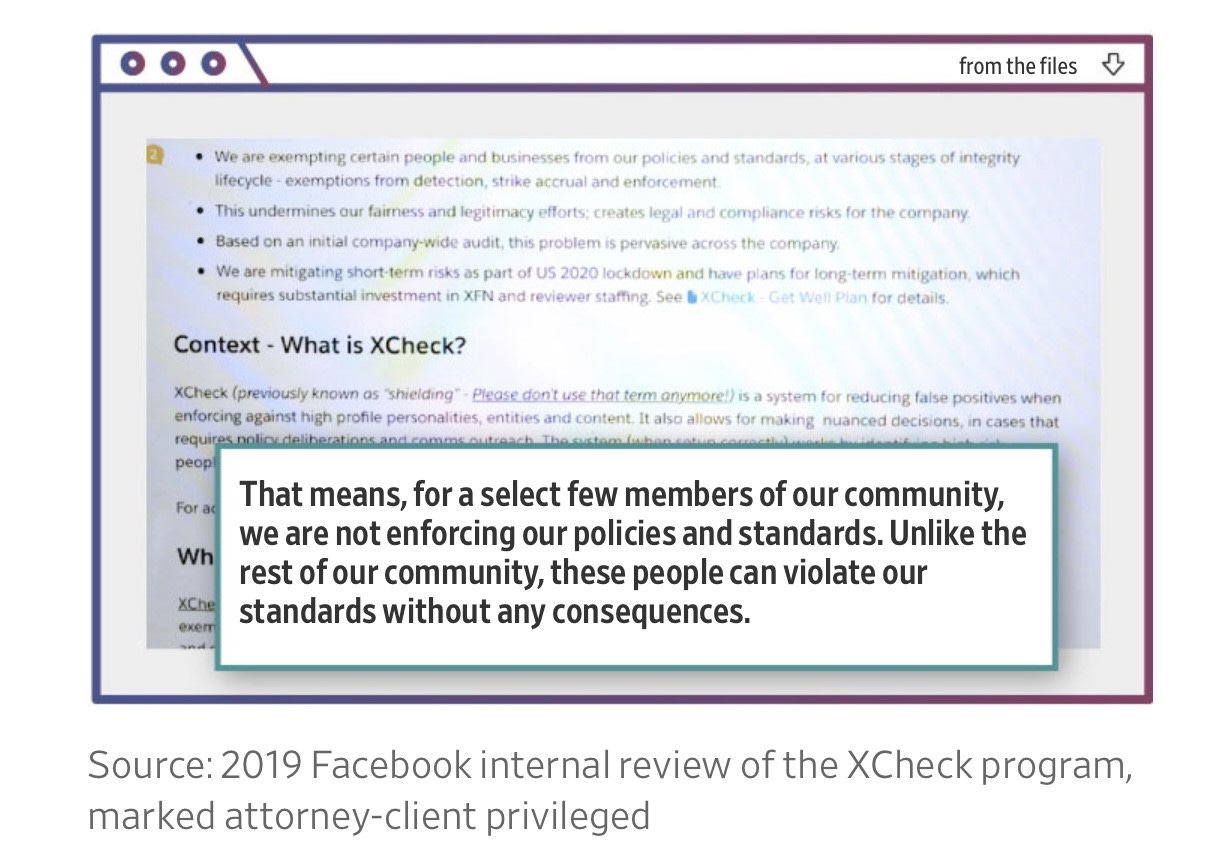

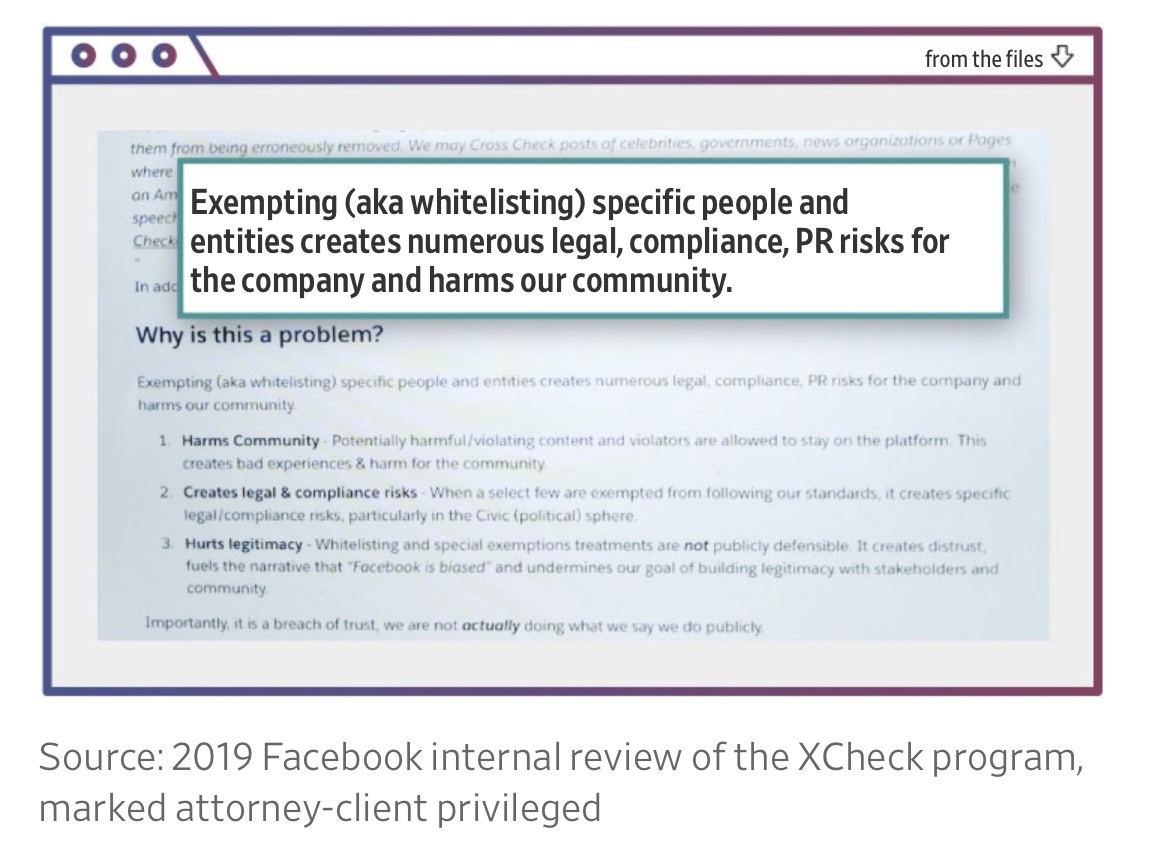

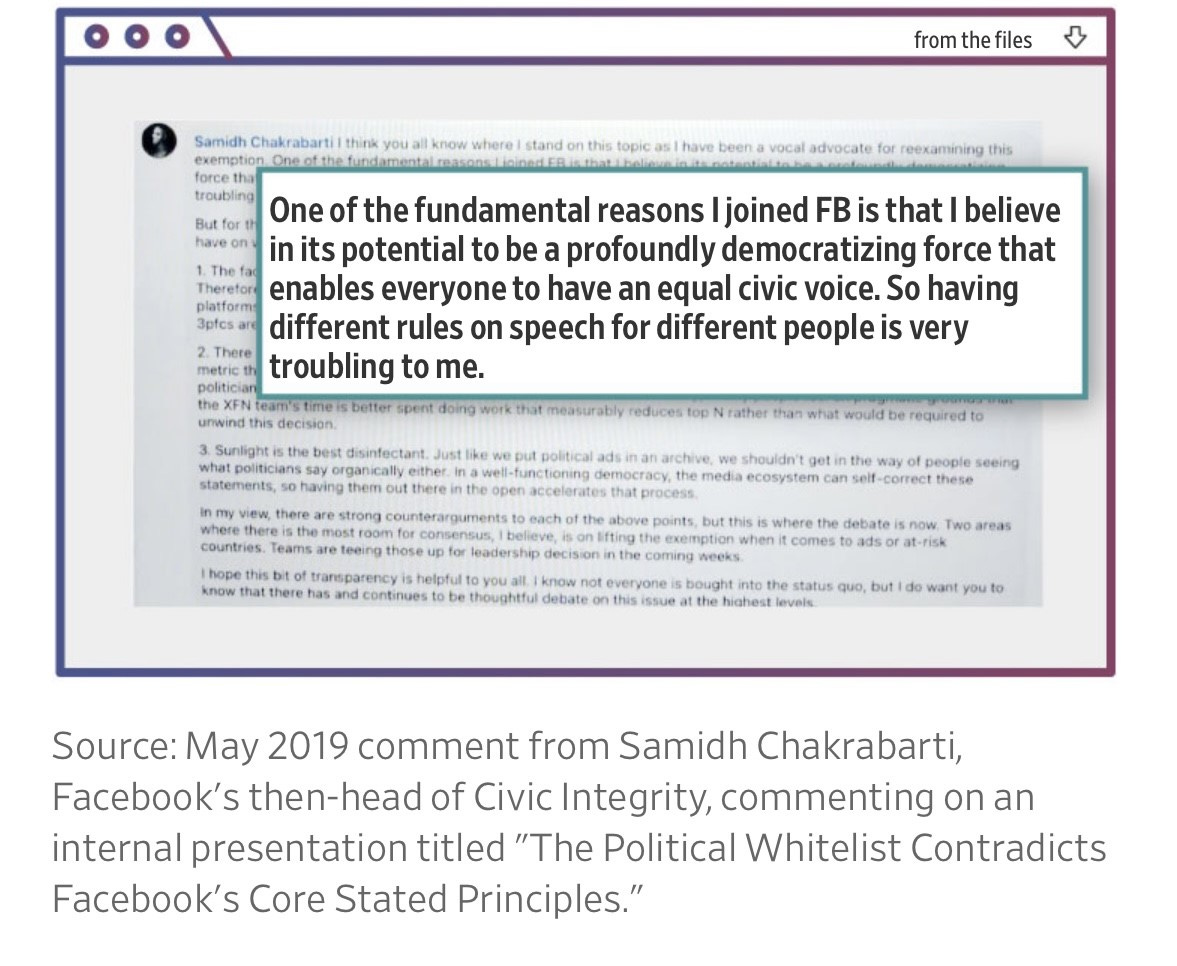

A powerful WSJ article which is quite critical of Facebook and the rule bending for VIPs. Mark Zuckerberg has publicly said Facebook Inc. allows its more than three billion users to speak on equal footing with the elites of politics, culture and journalism, and that its standards of behavior apply to everyone, no matter their status or fame. In private, the company has built a system that has exempted high-profile users from some or all of its rules, according to company documents reviewed by The Wall Street Journal. The program, known as “cross check” or “XCheck,” was initially intended as a quality-control measure for actions taken against high-profile accounts, including celebrities, politicians and journalists. Today, it shields millions of VIP users from the company’s normal enforcement process, the documents show. Some users are “whitelisted”—rendered immune from enforcement actions—while others are allowed to post rule-violating material pending Facebook employee reviews that often never come. A 2019 internal review of Facebook’s whitelisting practices, marked attorney-client privileged, found favoritism to those users to be both widespread and “not publicly defensible.” Below are pictures from the article. I have been critical of the power and platform given to Amazon, Google, Facebook and others. According to articles I read, Google has a roughly 90% search share and Facebook over 70% of social media. I feel very uncomfortable with this and strongly suggest my readers take a look at this article. Facebook is admitting rules don’t apply to all evenly. How Congress is not involved in making this right is beyond me. It is clear that the idiot politicians are in over their head on anything tech related. I am only asking for equal treatment. This is not a Red or Blue thing, it is about fairness and equal treatment in my opinion. Zuckerberg has too much power to influence outcomes and something needs to be done ASAP. Look at the three pictures below from Facebook. What do you think?

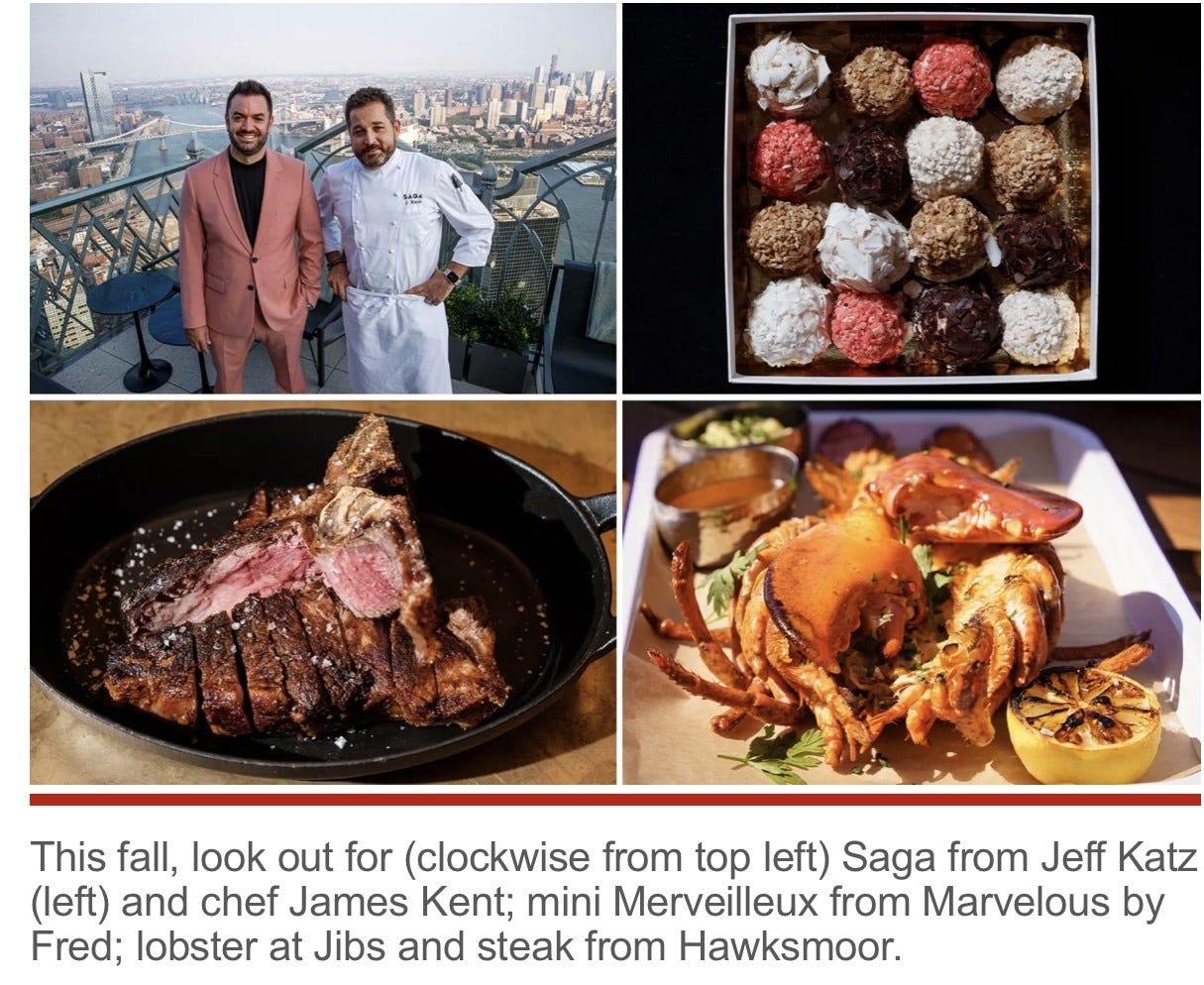

All the Rosen Report readers know about my love for food and great restaurant experiences, hence today’s theme section on sushi. This NY Post article outlines a bunch of NYC restaurant openings and re-openings as things are slowly getting back to normal. Some eateries mentioned in the article include: Marvelous by Fred, L’Appartement 4F, Patisserie Chanson, Breads, Jibs, Ci Siamo (Danny Meyer), Zou Zou’s, Kyma, Gotham (yes, same place without Portale), Torrisi Deli & Restaurant, Hutong, Una Picca Napolentana’s, Old Stove Pub (yes, from Hamptons), No.7 and many others are mentioned. I can’t wait to give some a try. I love Danny Meyer and Gotham was my old stomping ground. Many others look interesting to me. I can’t wait to get back to NYC for a few days and try a bunch of these places. Given the lower retail rents, less build out expenses and restaurant closures, I am hopeful the new establishments will have a chance to thrive The summer sun may be setting, but there’s lots on the horizon. After months and months of restaurant closures and uncertainty, things are on the upswing this fall with a flurry of exciting debuts. Old favorites are reopening, big-name chefs are making bold moves, fast casual is getting fancy, and carbs rule supreme. Have a look at the biggest trends and openings in the months to come.

The smoking of a powerful hallucinogenic toad venom in short retreats, a practice known as “speed-toading,” is exploding in the Caribbean tourist hub of Tulum, where it’s now a sought-after New Age healing tool. Bufo alvarius, which contains the fast-acting psychedelic 5-MeO-DMT—regarded by many as the world’s most powerful psychoactive substance—and often referred to simply as bufo, is touted by some of its purveyors as a miracle cure for the ills of the modern world and mental health issues. Ok, clearly I am a bit of a square. There is a ZERO percent probability of me going to Tulum to smoke toad venom. If any readers have done this, I would love to know about the experience. Will it help my back?

Virus/Vaccine

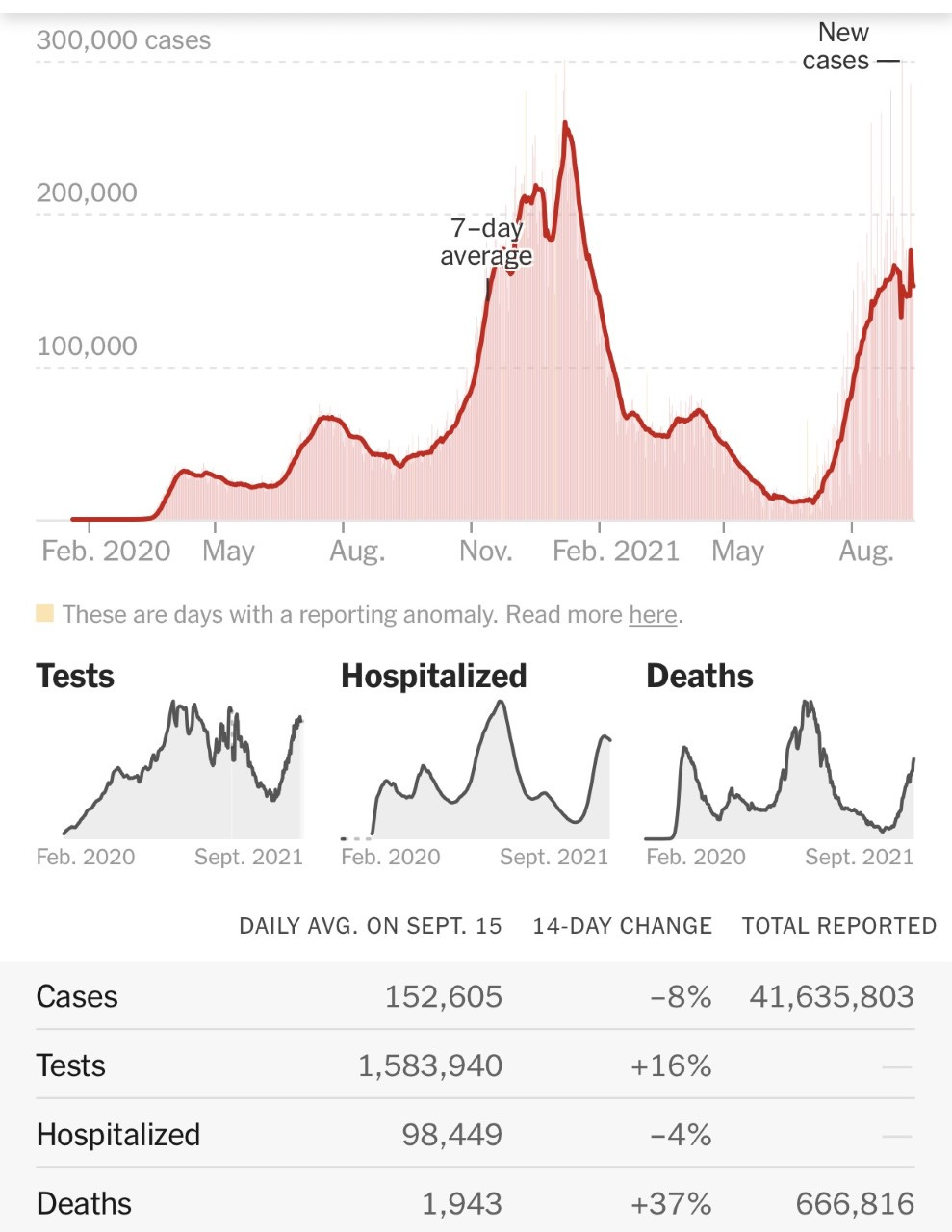

The improvement trend largely continues. Cases dropped 8% for the prior 2-week period and averaged 152k/day. Hospitalizations dropped 4% to 98k, while deaths grew at 37% (lagging indicator) to just under 2k/day.

Dr. Scott Gottlieb expects U.S. drug regulators to clear the Pfizer Covid vaccine for emergency use in children ages 5 to 11 in late fall or early winter of this year. The former FDA chief and current Pfizer board member told CNBC that such a timeline represents an “optimized scenario.” The spread of the delta variant may potentially pressure regulators to act more quickly, he suggested.

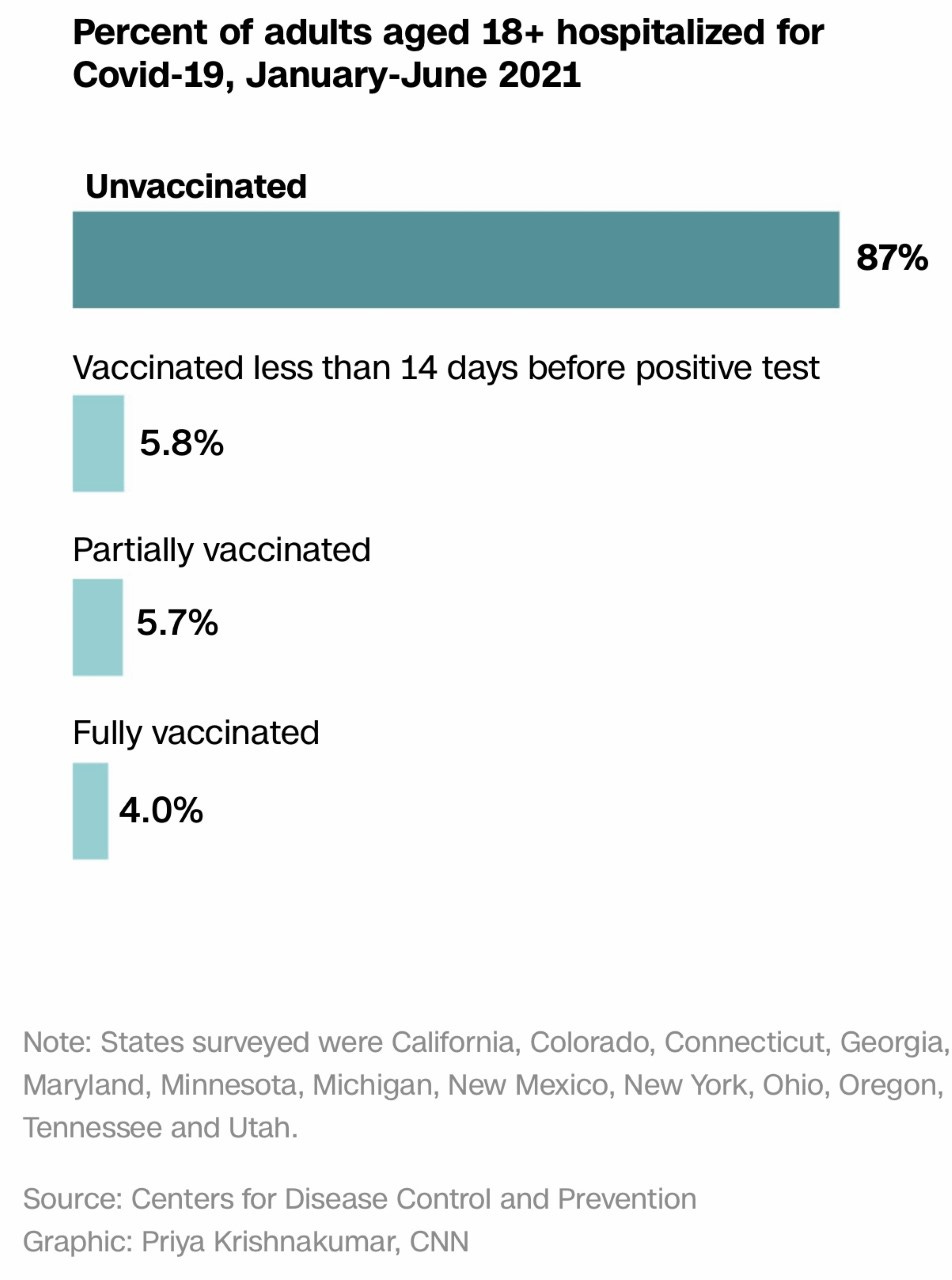

Remember, I am vaccinated. I am just suggesting that the vaccinations do not solve all the pandemic problems as seen in Singapore and Israel. I fear we will be living with COVID for years. Singapore is 81% vaccinated and is having record cases and a record number of people on oxygen. Similar stats in Israel as well on bottom of Singapore below. The rapid pace of new COVID-19 infections and a doubling of seriously ill patients in Singapore have raised unexpected hurdles to reopening plans for the vaccination frontrunner, where 81% of the population is fully vaccinated. Singapore, one of the fastest in the world to reach that level, has seen its inoculation rates plateau, and this month paused its gradual reopening plans, spooked by daily infections that returned to one-year peaks this month. Infections over the weekend were more than a combined 1,000 cases, a tenfold increase from a month ago. Many experts, though, are not overly concerned about the rise in infections because of the low number of serious cases and Singapore's high vaccination percentage. The number of patients requiring oxygen, however, doubled to a record 54 on Sunday from two days before, an important gauge to judge whether the medical system could get overwhelmed.

On Aug. 31, Israel registered 11,000 new Covid-19 cases, the highest daily number since the pandemic began. The worrying thing was: That day’s case count beat a record set in mid-January, when only a small proportion of Israel’s population had been vaccinated. By the end of August, at least 68% of Israelis had received at least one vaccine dose, but even the vaccinated were falling sick enough to need hospitalization. Alarmed, the Israeli government set about administering booster shots, trying to contain a surge in cases driven largely by the Delta variant of the coronavirus. In its speed and thoroughness, Israel’s vaccination drive was a shining model. But to other governments, Israel’s late-summer spike now presents the frightening prospect that vaccine immunity may wane quicker than expected.

Ray DeMonia wasn't seeking Covid-19 treatment when he arrived at an Alabama hospital with heart problems. But the 73-year-old became an indirect victim of Covid-19 patients filling hospitals and ICU beds. The cardiac patient from Cullman, Alabama, died in a Mississippi hospital about 200 miles from his home because there were no cardiac ICU beds nearby, his daughter Raven DeMonia told The Washington Post. In DeMonia's obituary, the family pleaded for everyone to get vaccinated to prevent others from being denied care due to a lack of resources.

Eighteen top scientists from across the world have warned against giving COVID-19 booster shots to most fully vaccinated people. In an review published in the Lancet on Monday, the experts said that the idea of boosting immunity to reduce COVID-19 cases was "appealing." But current evidence didn't support "widespread use of booster vaccination" in the general population, they said, citing 93 references. "Careful and public scrutiny of the evolving data will be needed to assure that decisions about boosting are informed by reliable science more than by politics," the review authors said. The group included Philip Krause and Marion Gruber, the two Food and Drug Administration officials who resigned over the Biden administration's booster shot plan earlier in September. I am not planning on a booster near term. I will re-assess a the end of the year.

Real Estate

My Thoughts

The influx of younger, successful people continues in the South Florida area. I met a great new friend this week. He’s in his late 40s and is a successful man who could no longer take the politics, homelessness or taxes of Southern California. He identifies as a Democrat. Another new friend was a hedge fund manager and now CEO who relocated from NYC to Florida with his young family. Another former hedge fund manager moved to Jupiter in a gated community. A former senior GS partner moved to Boca, and I recently confirmed a current senior Wall Street executive has kids enrolled in school in South Florida. These are not the type of people who have historically lived down here. Prior to the pandemic, these moves were a rarity, and now they are happening every day. If the higher end tax rates pass and NYC, CA and other high tax states continue to put even higher taxes on the wealthy, the flood to Florida, Texas, Wyoming and Nevada won’t be ending any time soon. There is an article citing South Florida is the worst area in the country to rent given 40-45% of income is being spent on rent given the substantial increase in demand. It is in the Sun Sentinel, but I am not a subscriber.

I was just told a house in Long Lake Estates (West Boca) was listed for $14.9mm. It is 12,000 ft on a little more than 1 acre and was built in 2007. The pictures look nice. I have no idea who would pay that much to live west. You can be on the water for around that price and this house is 10 miles to the beach. It is yet another sign of the market insanity. If it sells in the vicinity of $15mm, I will be blown away.

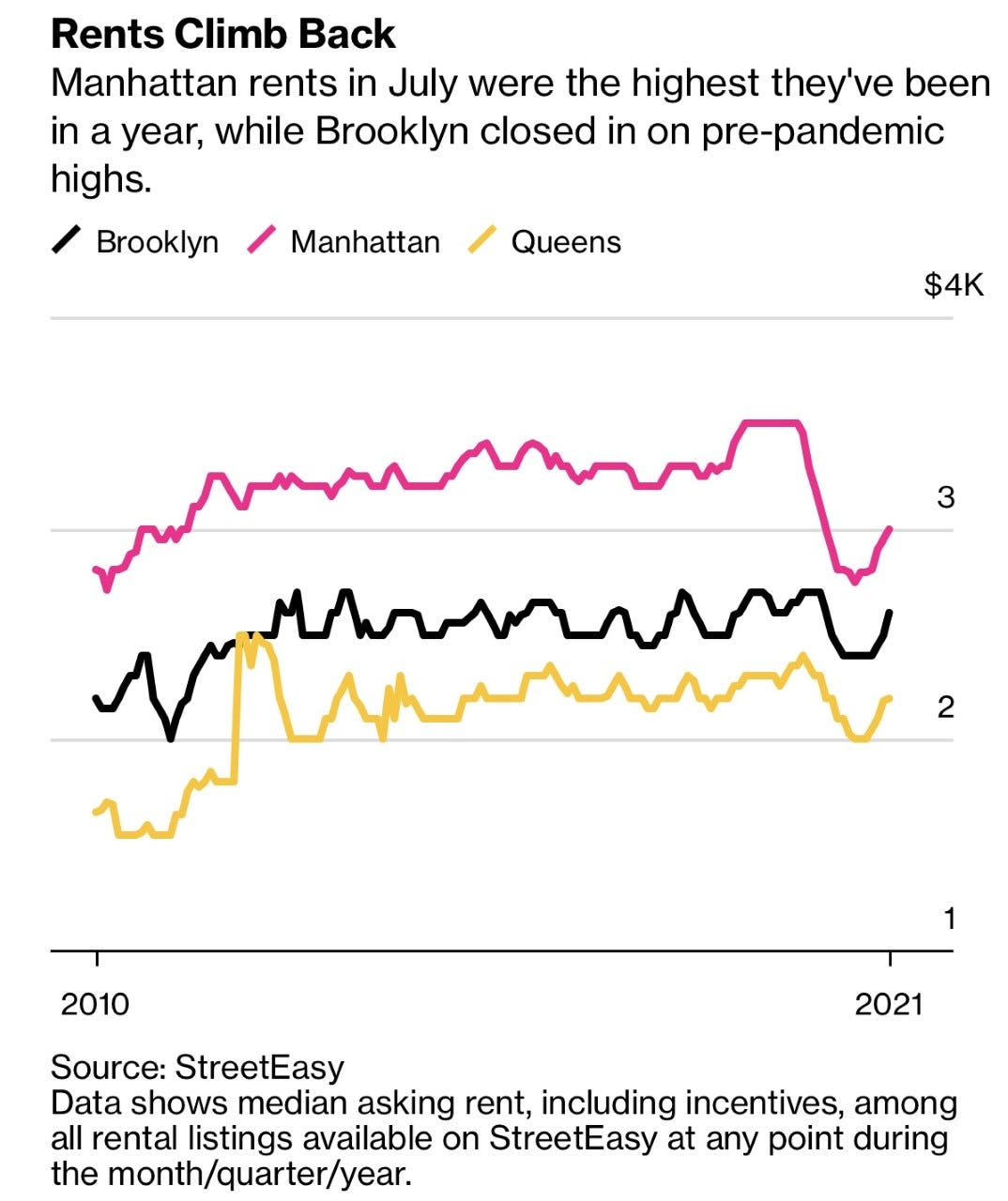

NYC Rents on the Rise

The pandemic-era rental market in Manhattan gave people the chance of a lifetime to move into the apartment of their dreams. Ten months is all they got. Landlords are jacking up rents — often by 50, 60 or 70% — on tenants who locked in deals last year when prices were in free-fall. Some renters are being forced to move at a time when the market is roaring back to nearly pre-pandemic levels. And concessions are slipping away.

Just after 9/11, no one wanted to live downtown and there were all kinds of limitations on being downtown due to air quality. I decided to move from the UWS to Greenwich Village in early 2002. I rented a 4 bedroom PH on 5th Ave & 9th Street for $7,500/month. It was too big for me as a single guy, but my mom was sick with cancer and was going to come to NYC for treatments and felt we needed space. She decided not to come to Memorial Sloan Kettering and I had this big apartment for myself. Prior to me, the tenant paid $20k. Shows what happened post 9/11. Within a year, it was clear I was massively underpaying. When my lease was up, they moved it to $12k, then $15, $20… I moved out 10 years ago. I would guess that just prior to the pandemic, it could have rented for $50k. I was lucky I had the foresight to lock in a longer lease at reduced rents.

JPM Research on Housing-There is No Place Like Home

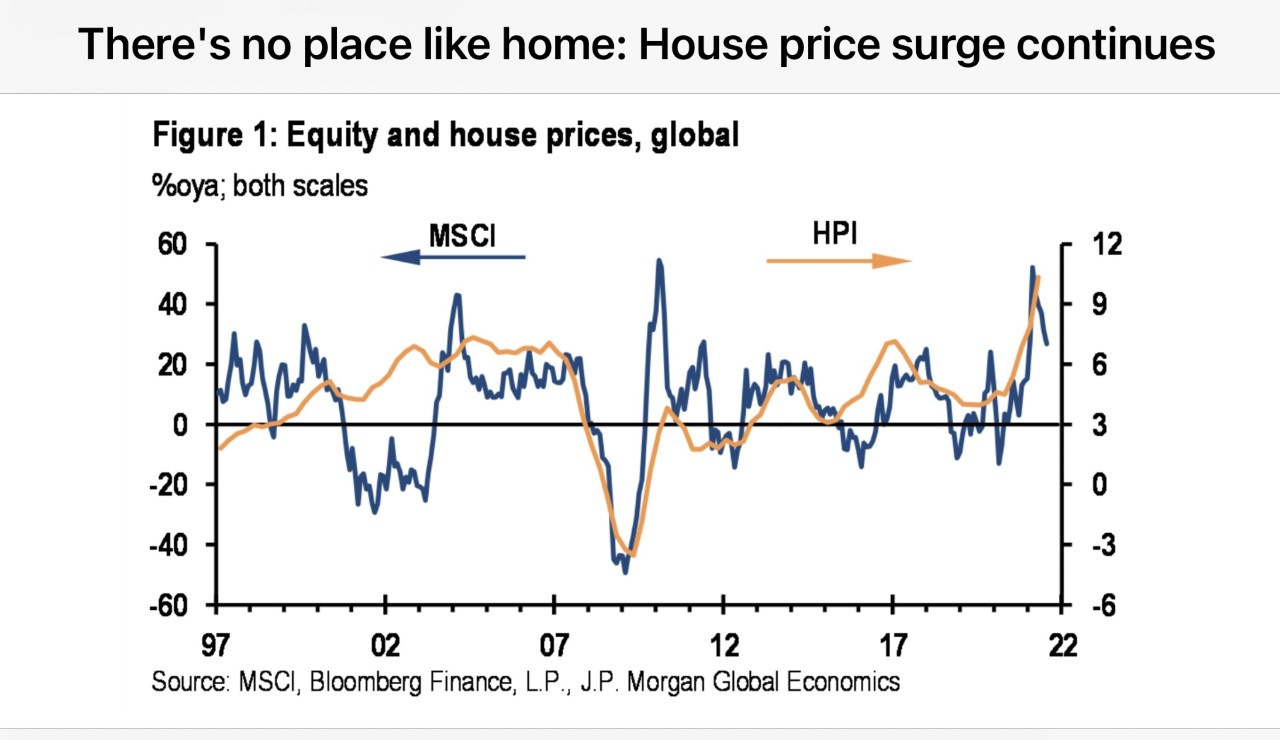

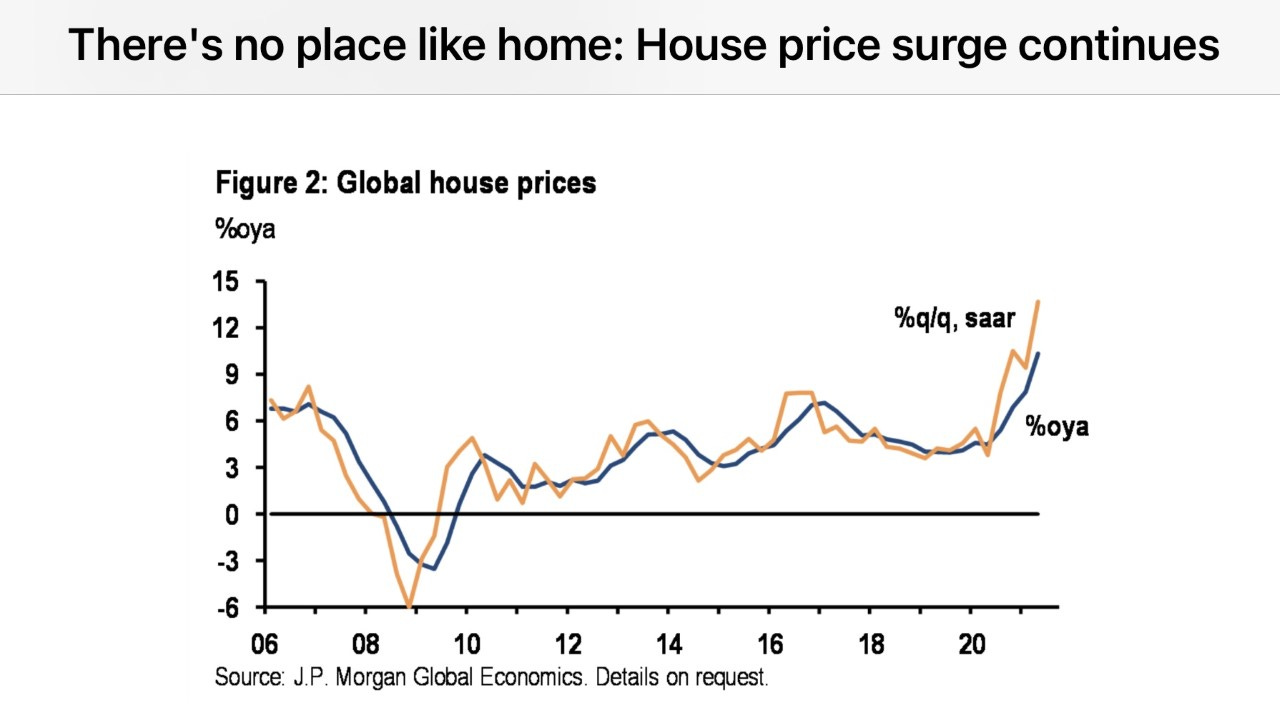

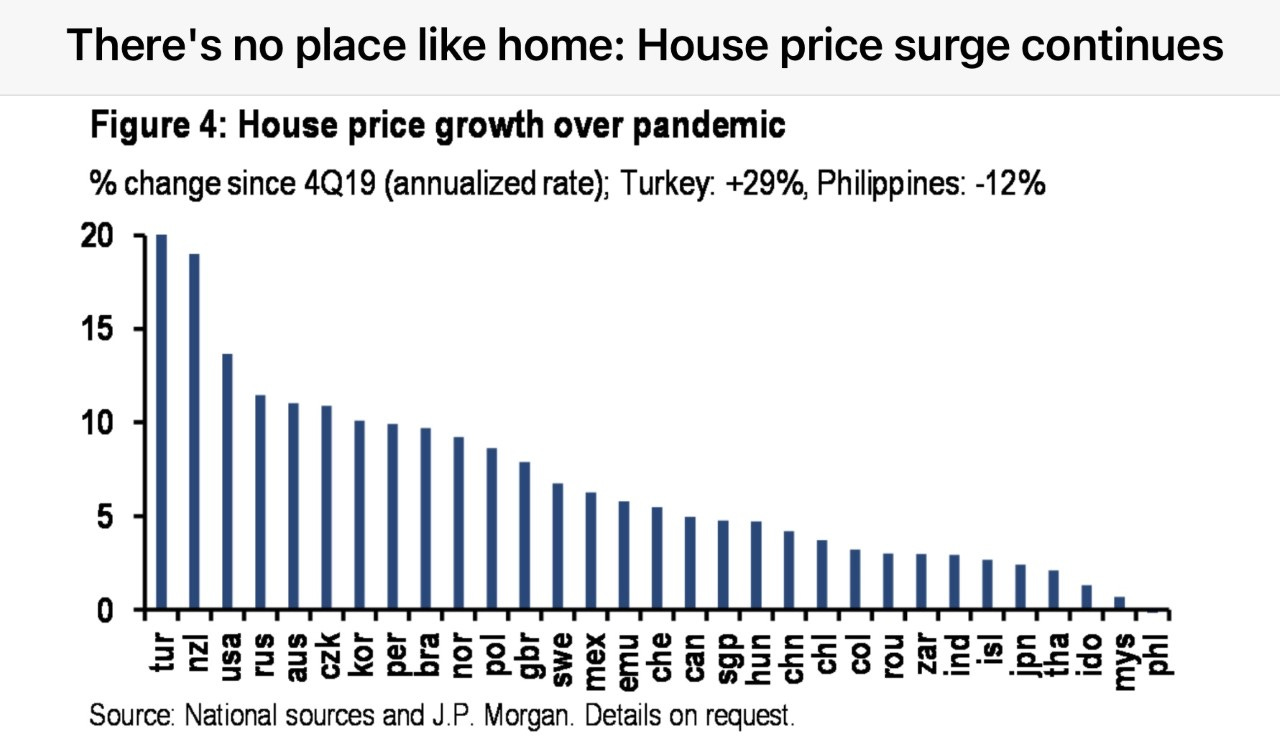

I read this JPM piece by Joseph Lupton and Bannet Parrish. I just took a few sections for you. I thought the chart by country was interesting. Seems like largely this the R/E game is hot not just in the US. In order to see the entire piece, you need to be a JPM customer.

The global economy’s dramatic recovery from the initial COVID-19 shock has been led by a remarkable recovery in asset prices. Global equity prices have surged and currently stand 33% above their pre-pandemic level. House prices have also registered large gains (Figure 1). In sharp contrast to the Global Financial Crisis (GFC), when house prices plunged through the recession, house prices never fell during last year’s downturn and have increased at a double-digit pace over the past year. As of 2Q21, house prices are tracking 13% above pre-pandemic levels.

While the pace of equity price gains appears to have slowed over the past two quarters house price appreciation continues to accelerate—tracking a 13.7% gain last quarter (Figure 2).

The pickup in house price inflation is broadly based, albeit with considerable variation (Figure 4). House prices jumped 12.8%oya in the DM last quarter against a 6.2%oya rise in the EM. Within the EM, EM EMEA house prices rose the most at 14.1%oya followed by Latam at 8.8%oya and EM Asia at 4.6%oya. The extraordinary gains are concentrated in several large economies. The US (17.6%oya) and the UK (10.5%oya) stand out in the DM. However, gains are intense across the Antipodes as well (Australia and New Zealand). In the EM, Turkey (28.4%oya), Russia (11.4%oya), Korea (10.1%oya), Brazil (9.7%oya), and Czechia (10.9%oya) have all seen huge gains. Despite an overheated property market, price controls have kept house price appreciation in China in check.

UK Home Prices

That’s up from the estate agency’s prediction of 4% growth earlier this year, which was made before the extension of the stamp duty holiday, a government incentive that allowed buyers up to £500,000 (US$694,200) in transfer tax relief through June and will taper off completely in September.

Transaction volumes in 2021 are on track to reach 1.62 million, which is 35% higher than the average of the five years before the Covid-19 pandemic, the data showed.